are you investing, or cosplaying financial stability?

I did everything “right”. And still got it completely wrong.

Happy Sunday financial hotties!

This week, we’re getting personal about my investing regrets. How I did everything right, and followed every Financial Hot Girl philosophy ahead of time… but still got it completely wrong.

Before I start, here’s a quick refresher on my financial timeline, back to when I read my first personal finance book:

Age 24: Drowning in debt and living for payday

Age 25: Became debt-free and started investing £50/month

Age 26: Salary jump to £36k; investing £500/month into an index fund

Age 27: Same routine, consistent investor mindset

Age 28: Quit corporate, paused investing, lived off savings

Age 29/30: Paying myself through my business, rebuilding savings for travel

Now that you’re caught up (albeit briefly), here’s why I feel regret when I think about what I should’ve done at age 24.

I don’t regret investing. I regret investing as if I was going to stay in corporate forever. Because investing requires committing to a lifestyle, and I was committing to the wrong one.

Disclaimer: this issue is absolutely not a fear-mongering post about investing. Investing is a powerful, smart way to grow your wealth, give you options, and ultimately freedom. You’ll understand everything if you read this issue fully, so please do.

The version of me I was investing for

At 24 years old, I was a shy, new graduate in the thick of an intense job and accounting exams.

My career goals at the time were to make manager, maybe someday make partner, and then if—only if—I had the time and money, set up my own business in my 50s.

Content creation and being a self-employed creative were things I knew about, but never, ever considered as a path for myself.

I mean c’mon, at 24 I barely plucked up the courage to post my first YouTube video. Three years later, I was getting paid for it, and still hiding it from my colleagues.

The illusion of “doing everything right”

Thinking that I had at least 25 more years of the corporate hamster wheel to go, I tackled my personal finances from that point of view.

I built my financial plan around a life I didn’t actually want.

I invested at a set percentage every month, I kept my costs low and I devoted a good amount of energy to that yearly promotion.

But as soon as I got my first brand deal, I was quick to set up a limited company. Something in me, perhaps subconsciously, knew that this could be bigger than anything I could imagine at the time, so I separated everything. I didn’t just treat it like a side-hustle.

Ironically though, I still didn’t fully embrace being a creator. If I had simply had more trust in myself, and more faith in my future, I could have started saving for a career pivot at 25 instead of committing to investing aggressively and acting like a business was reserved for my 50s.

I’d already Decided Once—a Financial Hot Girl micro-philosophy—but just for the wrong thing.

I decided on a corporate path, a strict budget, and an investment plan that assumed I’d stay in that life for the next 15+ years.

The power of deciding once only works when you’re honest about what you’re deciding for.

What nobody tells you about long-term investing

When I was investing £500 a month, I wasn’t just investing in my index fund—I was investing in a version of myself that didn’t actually exist yet. The corporate Dev who’d stay at Deloitte for decades, get promoted every few years, and retire with a nice pension.

Deep down, I knew that wasn’t me. I was pouring money into a plan that didn’t fit the lifestyle I actually wanted, but was too scared to commit to.

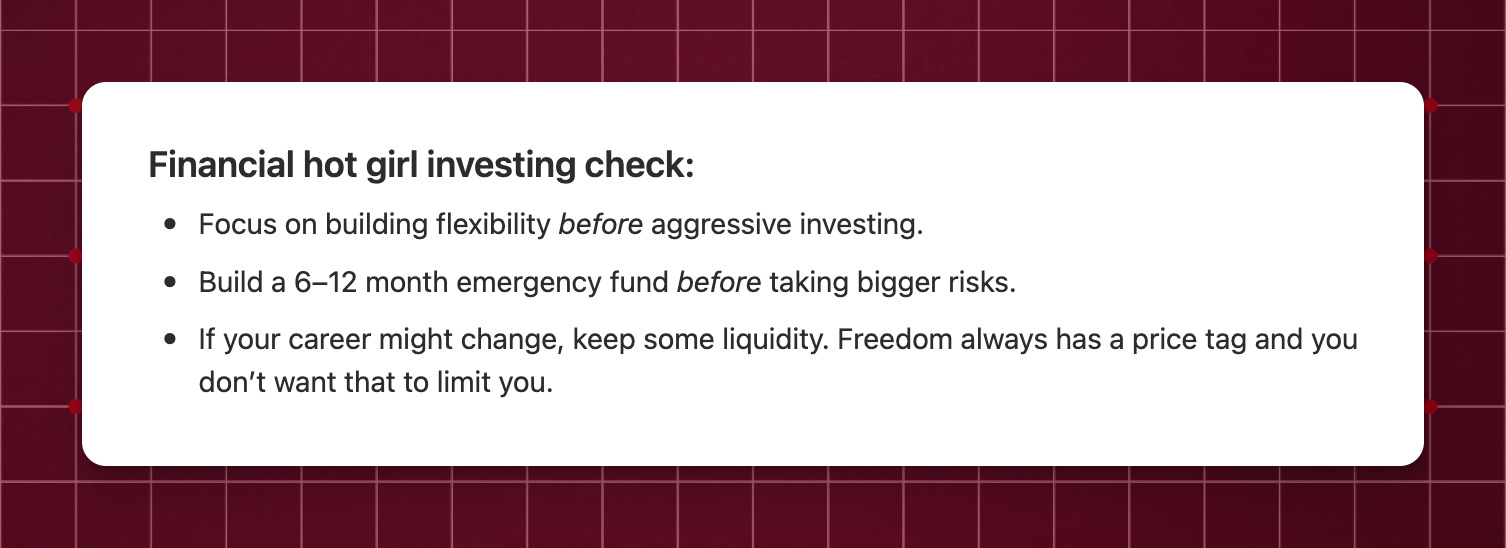

Investing is a long-term commitment. Not just financially, but psychologically. You’re committing to a certain way of living for at least 10–15 years. And if that lifestyle changes, your investing strategy has to change too.

If your lifestyle or income changes, revisit your investing approach. A few questions to ask yourself:

Is my income stable enough to keep investing monthly without stress?

Am I building enough cash buffer for the life I’m living now?

Do my investing goals still match the lifestyle I’m working towards?

For business owners or freelancers, a bigger financial cushion is compulsory. It gives you the stability to create, experiment, and take risks without panicking.

It’s something I wish I’d realised earlier. I knew it intellectually, but didn’t have the courage to take that path on myself.

The money I invested could’ve bought me time and freedom sooner—the very things I was chasing through corporate promotions.

The real cost of not trusting yourself

I don’t regret investing. It taught me discipline, gave me financial literacy, and confidence. But I do regret not trusting myself sooner.

I know some of you reading this are in that same in-between land. Dreaming about the freedom to build a life you want, but terrified to give up stability.

Now, I invest differently—from alignment, not obligation to a life I thought I needed. I still know and believe investing is how you build long-term wealth, but I also believe how you earn the money you invest matters.

Financial freedom still requires commitment. The question is: what kind of life are you committing to in the process? That’s the real Financial Hot Girl mindset.

Until next week,

—Dev xo