why you're not unlucky with money

the world is reaching into your account whether you're watching or not | fhg #84

One thing before we start! The conflicts I mention in this issue are real and still unfolding, and I want to be clear that I’m not treating them lightly. I don’t want to reduce them to a finance lesson. People are being affected in ways that go far beyond the cost of a flight. I just think you deserve to understand how these things connect to your actual life, and how you can use that knowledge to do better things with your money.

Happy Sunday financial hotties. As you know, I’m currently travelling in South America, and this week someone I met on the road said something to me that I couldn’t stop thinking about.

We were talking about travel plans and I mentioned I needed to book my flight home soon. They said: “you might want to do that soon, if the Iran situation escalates, oil prices will go up and your flight will get more expensive.”

It made me stop and think — if I hadn’t spent the last few years obsessing over money, would I have had any idea why flight prices went up? Probably not. And that matters, because when you don’t understand why your cost of living keeps creeping up or why your mortgage rate won’t drop, it just feels like the world is something that is constantly happening to you. You feel unlucky or worse, bad with money.

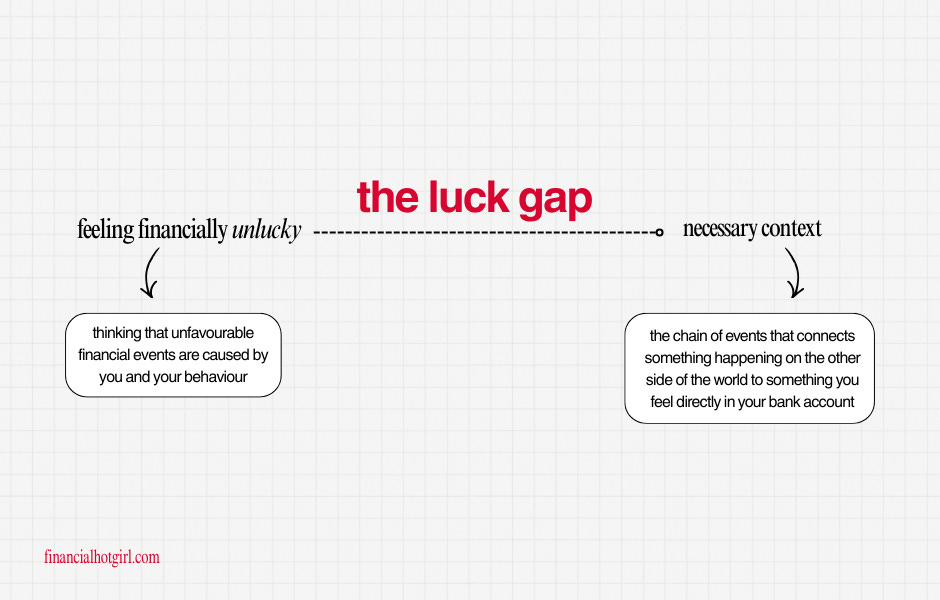

Thankfully, luck has no place here. All that’s missing is context. I call it the luck gap: the distance between feeling financially unlucky and actually just missing context — and closing it starts with understanding the chain: the sequence of events that connects something happening on the other side of the world to something you feel directly in your bank account.

𝜗ৎ In this issue:

What the chain actually looks like

How to close the luck gap

What the chain actually looks like

Here are three examples of that chain in action right now.

Example 1: Your food shop

Right now, there is war with Iran. The Strait of Hormuz (a narrow waterway off the coast of Iran) is where roughly 20% of the world’s oil supply passes through every single day. Since the conflict began, that waterway has been effectively paralysed, and oil prices have surged to near $120 a barrel, the highest since 2022.

When oil gets more expensive, diesel gets more expensive. More expensive diesel means higher delivery costs for every product that needs to get from a farm or factory to your local Tesco. On top of that, fertiliser is made from natural gas — the price of which has also spiked — meaning it now costs farmers more to grow the food in the first place. Both of those costs end up on the shelves of supermarkets.

Energy prices are the thread that runs through the entire global food system, and straight into your basket during your Sunday food shop.

Example 2: Your subscriptions and lifestyle costs

When oil prices spike, inflation rises across the board. The things that cost businesses more — energy, transport, materials — get passed onto us. And subscription businesses are no exception. Your gym, your streaming services, your phone plan, all of these companies face higher operating costs during inflationary periods, and the way they protect their margins is by raising your monthly fee.

A £2 or £3 increase individually feels like nothing, but collectively they are a very real drain on your monthly budget that has nothing to do with your spending habits and everything to do with the macroeconomic environment we’re living in. But the false belief of thinking it’s you that’s the problem is why it’s important to understand where in the chain these financial changes happen.

This is also why inflationary periods are actually the best time to audit your subscriptions — not to cut everything, but to make sure you’re actively choosing what stays rather than passively letting price increases accumulate.

Example 3: Your rent

Rising rent is a structural problem in most places, that goes beyond any one conflict. But the macroeconomic environment absolutely makes it worse.

When oil prices spike, inflation goes up, and the Bank of England faces a choice about interest rates. Higher interest rates make it more expensive for landlords to hold mortgages on rental properties, and many of them pass that cost straight on to tenants through increased rent1.

So when your landlord puts your rent up and it feels completely disconnected from anything you’ve done...it often is. You didn’t cause it. But understanding why it’s happening means you can plan around it rather than just absorbing it and feeling stuck.

The average monthly rent in the UK is now £270 more than it was in 2020. That is not a coincidence. That is the downstream consequence of a pandemic, an energy crisis, a war in Ukraine, and interest rate decisions made in response to all of it. All of those things reached into your life and your bank account without asking.

A result of the chain, and not your luck.

How to close the luck gap

One thing I really didn’t want you to take away from this issue is that you need to obsess over geopolitics or economics in order to understand your money. There is a link, but you don’t need to be an expert at describing it.

I do, however, think there are 3 shifts that separate someone who feels at the mercy of their finances from one who feels like they’re playing a different game completely.

1. Start reading the news as a financial feed

Build your context! When something big is happening in the world, get into the habit of asking one question: where does energy touch this? Oil, gas, and food are the first dominoes in almost every cost-of-living shift. If you can spot the chain early, you make decisions ahead of the curve rather than reacting to the consequences.

2. Build a buffer that isn’t doing nothing

An emergency fund in a high-interest savings account at least keeps up with some of inflation while it sits there. It also acts like a shock absorber when there is volatility in our lives and in the world. Money sitting in a current account is losing value whenever inflation is running high.

3. Stop confusing ‘bad’ timing with ‘bad’ habits

This is the one I really want you to take away. If your cost of living has gone up, if your rent keeps increasing, if your subscriptions keep creeping — that is not a reflection of how good you are with money2. Knowing the difference between a structural problem you can fix and an external one you can only prepare for is one of the most underrated financial skills there is. And it starts with understanding the chain.

Your money is not separate from the world. It never was.

The Financial Hot Girl way of thinking about it is this: luck is just a word we use when we don’t understand the chain yet. The more you close that luck gap, the more context you have, the less your financial life will feel like something that just happens to you, and the more it will feel like something you’re actually ahead of.

That’s what financial confidence actually is, knowing enough to stop calling it luck.

See you next week,

— Dev xo

A note on accuracy: The oil price figures and Strait of Hormuz details are based on real reporting as of this week (March 2026). The Iran-US conflict is ongoing and the situation is developing, prices and timelines may shift by the time you read this.

Average UK private rent has increased 3.5% in the 12 months to January 2026, and has been outpacing wage growth for the better part of two years (!)

This is all provided that you monitor your spending enough that you know your subscriptions, their costs, etcetera.

Excellent read and easy to comprehend! Thanks for sharing.

I like the reminder to learn enough about what's going on in the world to become proactive instead of reactive to price increases.